Even before the advent of MTD, using a VATcontrol account assisted in maintaining the integrity of the accounting system. Using a VAT Sales and purchases account would still allow you to calculate the correct figures but without it clearing to a separate nominal code you will not have that final lock that would give you the total that is owed (or owing). In doing so it would also provides a detailed breakdown of what those figures in case you were ever audited.

We all know that VAT is a consumption tax. It is a percentage that is added any product or service sold or consumed within a geographical territory. In the US it called sales tax, in Australia and in other Asian countries it is called GST (goods and services tax) but basically it is the same thing. It is popular with governments as it is seen as fairer method as everyone pays and the wealthier tend to buy larger value ticket items so they pay more where those on more modest means don’t consume as much, so they pay a bit less. It is very difficult to avoid compared with other tax schemes. It is also easier for the public to accept as they assume it is on everything, where PAYE you see how much is deducted at source and inheritance tax is seen as deeply unfair as it seems to take away your rewards at the end of your life.

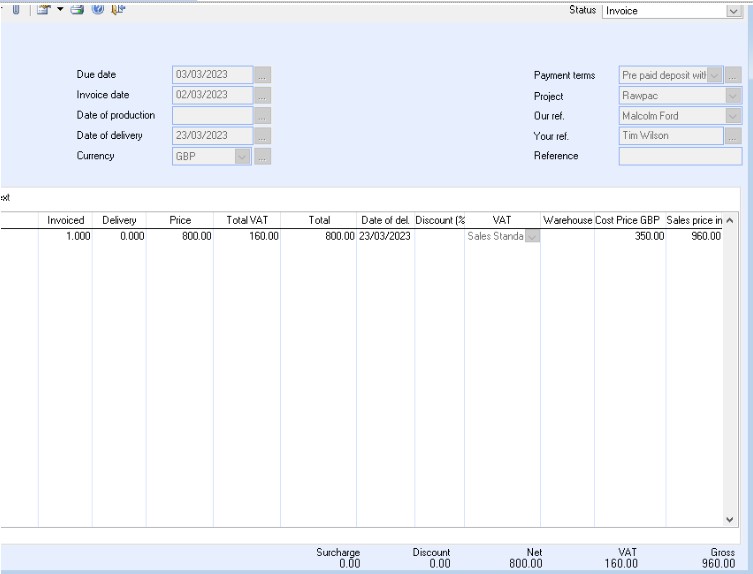

To see it in operation every Sales invoice that is raised (as long as the entity is registered) VAT is added to the nett amount. For the UK the rate is 20%.

This creates a sales journal in the accounting system. Notice that the nominal code for VAT on sales is on the credit side. This records that this amount is a liability and is owing to the government of the day.

![]()

The date of this transaction is held within an accounting period which is normally defined by the month that transaction is raised, but not always. More on that later.

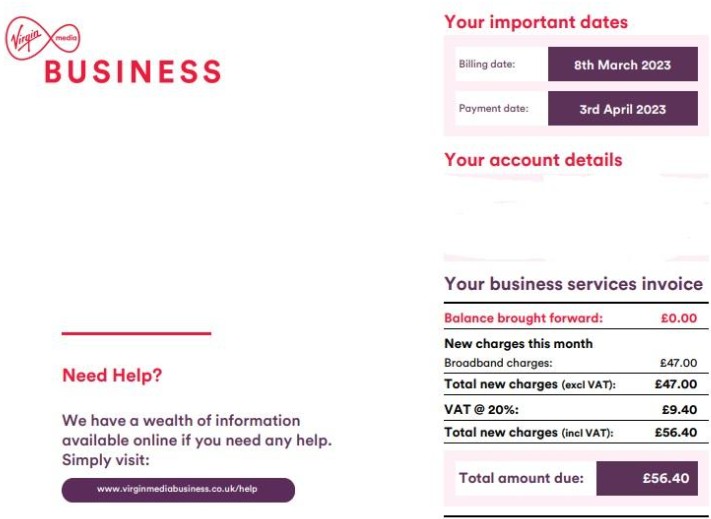

The other side of the equation is that a business can reclaim from any purchase invoices you receive from a Vatable entity. These amounts reduce whatever liability has been built up in the previous VAT sales nominal code. Below is an example of a purchase you may have made and the VAT element applied. The total is what you pay to your supplier and in turn, that is a sales invoice from their perspective and they then pay the government out of the amount you have paid them.

Purchase invoice with VAT

Once you post that in your accounting system this creates a purchase journal but this time the VAT is in a different code for VAT on purchases. Notice that this a debit, meaning an asset and therefore reduces the amount payable in your return.

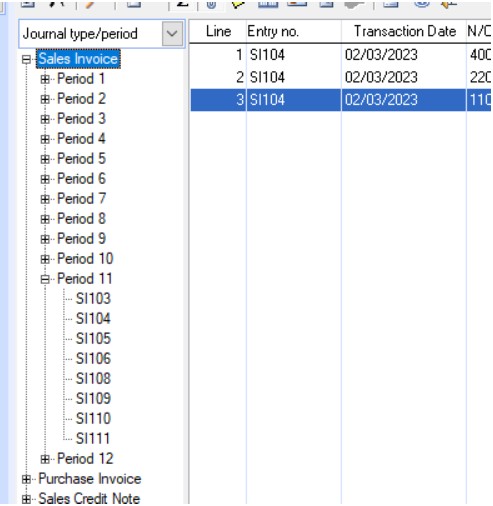

The transaction is also in a purchase period and if both transactions are in the same VAT Period they are then reported on the next VAT return.

![]()

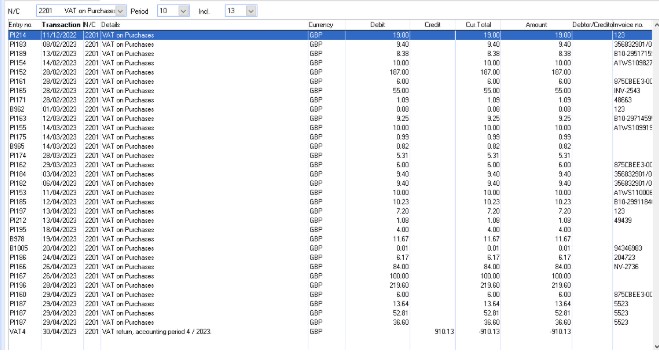

At the end of that VAT period (usually a quarter, but may vary) all the amounts within our VAT on Sales account are tallied up to get a final amount. Notice the debit at the end where the total amount is removed from that nominal code.

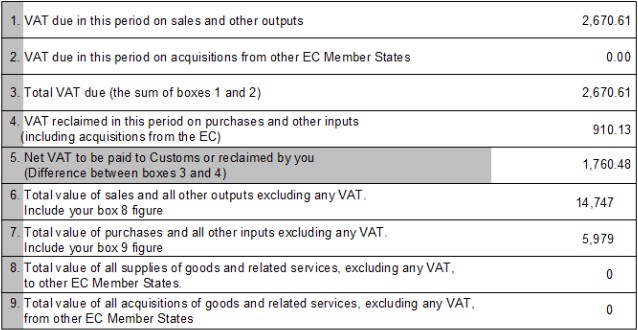

This is the same figure that appears on the VAT report.

When the VAT period is closed the final sales on VAT figure and in the purchase Nominal ledger will be calculated and the balance placed in a 3rd nominal code called VAT liability. The previous nominal code will be set to zero to begin capturing transactions for the next VAT period.

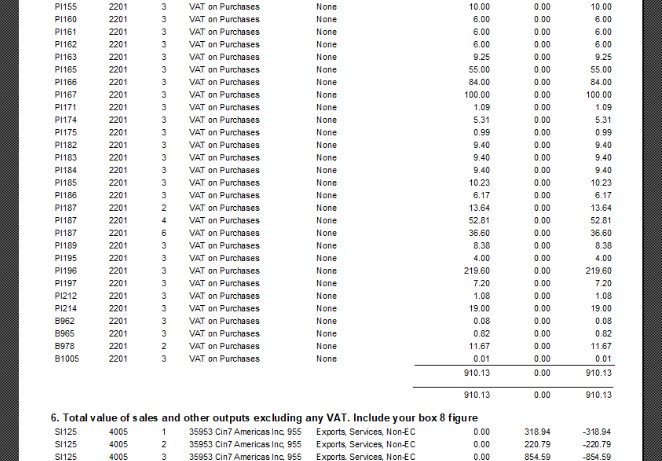

The VAT details report will record all the transaction that relate to these nominal codes and which box on the report they relate to. This important to keep as it will be used if you are ever audited by HMRC.

About the author:

Malcolm Ford worked as an accountant in the media industry before transferring his skills on to systems. He now works as an advisor for business’s who wish to upgrade their ERP and WMS software particularly working with those affected by the removal of support for Exchequer software. (https://it-ebs.co.uk/)